When it comes to any mobile app, we often think of it as a single-purpose solution, for example, for payments, education, or commerce. But the advent of the top super apps, like WeChat or Shopee, has shifted this mindset, surprising many people with a unified platform that can serve many purposes without the need to leave the app.

When user demand for gathering services in one place increases, super apps become more popular accordingly, and of course, become one of the mobile app development trends. What are the best super apps to consider? What do they serve for? Don’t skip this article, as it offers all the basics about this tech trend.

What Is a Super App?

At its core, a super app is a unified mobile application that offers various mini apps for different services, from messaging, e-commerce, payments, transportation, and even games.

The founder of BlackBerry, Mike Lazaridis, coined the term “Super App” in 2010 at Mobile World Congress. But it truly blossoms in Asian markets, with big names like Shopee, Grab, WeChat, and Momo.

Super apps grow, as they offer undeniable benefits to users. There’s no need to install too many apps (that significantly consume your phone’s computing power) or to switch between different apps. Instead, super apps bring unparalleled convenience by integrating all the services you need, from a trusted payment wallet to e-commerce stores, in one place. One big plus is that you can accumulate and use points from one service to exchange for discounts on another.

Super apps also benefit businesses. Inevitably, they enable businesses to approach a wider audience who use different services. This also allows businesses to learn more about their users’ habits and preferences across different verticals, hence offering highly personalized services. All these reasons make super apps so popular, especially in the Asian region.

Top 15 Super Apps in the World

Wonder which super apps are dominating the world? Let’s discover the top 15 super apps that consolidate messaging, payments, commerce, and other services:

1. WeChat (China)

- Country of Origin: China

- Key Features: Messaging, social networking, mobile payments (WeChat Pay), ride-hailing, food delivery, utility bill payments, mini-programs (third-party services), news feeds, gaming, e-commerce.

- Number of Users: Over 1.4 billion monthly active users globally as of October 2025

- Revenue: Around $62 billion in 2024

The first, and also most popular, super app in this list is WeChat. Those outside of China often consider WeChat as more or less a messaging app. But in fact, WeChat offers more than that, from chatting with friends and family to paying for a street vendor’s noodles or even luxury goods – all can be done via WeChat.

WeChat acquires its super app royalty status due to its incredible ecosystem of “mini-programs.” These bite-sized applications run within WeChat, without the need to be separately downloaded. So, you can order a taxi, book a doctor’s appointment, play a game, or even invest your money, all without ever leaving the WeChat interface.

2. Alipay (China)

- Country of Origin: China

- Key Features: Mobile payments, online banking, wealth management, insurance, credit scoring (Zhima Credit), utility payments, ride-hailing, food delivery, travel booking, e-commerce integration.

- Number of Users: Around 704 million monthly active users as of May 2025

- Revenue: Around $25 billion

If WeChat is the social heart of China’s digital world, then Alipay is its financial backbone. These two are often seen as rivals, yet they both carved out their own colossal niches.

Alipay, originally born out of Alibaba’s e-commerce needs, has changed into this incredibly powerful, standalone financial super app. It’s pretty much the go-to for payments in China, right alongside WeChat Pay. The introduction of Alipay really did help push China into becoming a virtually cashless society.

But here’s the thing about Alipay: it’s not just about scanning a QR code to pay for your groceries, although it excels at that, for sure. It has created an amazing array of financial services that genuinely empower users. From micro-loans and wealth management products to insurance and even a personal credit scoring system called Zhima Credit, Alipay really puts a vast pool of financial tools right in your pocket.

3. Grab (Southeast Asia)

- Country of Origin: Singapore (serving primarily Southeast Asia)

- Key Features: Ride-hailing, food delivery (GrabFood), package delivery (GrabExpress), mobile payments (GrabPay), financial services (lending, insurance), grocery delivery, hotel booking.

- Number of Users: Over 46 million monthly transacting users (MTUs) in 2025

- Revenue: $873 million in Q3 2025

Grab is the top super app in Southeast Asia. Started out as a ride-hailing service, kind of like Grab initially debuted as a ride-hailing service, like the Southeast Asian version of Uber. But it didn’t just stop there. Instead, it just kept growing into what local people actually need.

What’s impressive is how Grab managed to weave so many services together into this single, unified platform. From getting your late-night dinner delivered to sending an urgent package across town, all is managed within one app. It also integrate its own digital wallet, GrabPay, which ties the entire thing together financially and make cashless transactions almost effortless.

4. Gojek (Indonesia)

- Country of Origin: Indonesia (serving primarily Southeast Asia)

- Key Features: Ride-hailing (motorcycles and cars), food delivery (GoFood), logistics (GoSend), mobile payments (GoPay), financial services, on-demand services (massage, cleaning), entertainment booking.

- Number of Users: Around 38 million active users

- Revenue: Roughly $1.1 billion as of September 2025

Gojek is another noticeable super app dominating Southeast Asia. Much like Grab, it originally focused on motorcycle ride-hailing, considering the infamous traffic in Jakarta, but it has since truly evolved into a comprehensive super app, and it’s fiercely competitive with Grab in many markets.

Gojek offers an incredibly diverse range of on-demand services. Beyond just your typical rides and food delivery as the baseline, Gojek lets you book a relaxing massage (GoMassage), find house cleaners (GoClean), and even hire a mechanic (GoFix) right through the app.

Its digital wallet, GoPay, is an outstanding component of Gojek. You can use GoPay to pay for everything from that GoRide to the GoFood delivery, so it essentially becomes an indispensable tool for millions of people navigating their daily lives and finances.

5. Paytm (India)

- Country of Origin: India

- Key Features: Mobile payments (UPI, wallet), online banking, bill payments, ticketing (movies, travel), e-commerce, financial services (loans, insurance, mutual funds), wealth management.

- Number of Users: Approximately 72 million monthly active users in 2025

- Revenue: Around $761.8 million in 2025

Heading over to India, we absolutely have to talk about Paytm, owned by One97 Communications. This super app has been a real game-changer for digital payments in the country, especially with the massive push towards a cashless economy. Originally starting as a mobile wallet, Paytm has then expanded its horizons to become this incredibly comprehensive platform that handles everyday financial transactions for millions of Indians.

What’s pretty significant about Paytm is its deep integration with India’s Unified Payments Interface (UPI), which has totally revolutionized digital transactions there. This means users can pretty much pay for anything, anywhere, almost instantly, directly from their bank accounts via Paytm. But it’s not just payments; Paytm offers a really robust suite of financial services, from investment opportunities and insurance to loans and even ticketing for movies and travel.

6. Kakao (South Korea)

- Country of Origin: South Korea

- Key Features: Messaging, Kakao Pay (digital wallet/finance), Kakao T (taxi/transportation), Kakao Friends (e-commerce/gifting), Kakao Bank (online banking), content and gaming services.

- Number of Users: Around 54 million monthly active users globally

- Revenue: Over $1.4 billion in Q3 2025

KakaoTalk, or Kakao, is a popular messaging app in South Korea. People may miss this one in the global lineup, but in Korea, if you’re not on “Kakao,” you basically don’t exist digitally.

Kakao has deeply woven itself into the national infrastructure. Take Kakao T, and you can hail a regular cab, a luxury car, or even an agent to drive your own car home for you after a late night. Then there’s Kakao Pay and Kakao Bank, which really do rival traditional financial institutions. The gifting feature, where you can send a friend a coffee coupon or a physical product right through the chat window, is huge.

7. LINE (Japan & Asia)

- Country of Origin: Japan

- Key Features: Instant messaging, voice/video calls, LINE Pay (digital wallet), LINE Manga/News, sticker creation/sales, Official Accounts, e-commerce (LINE Shopping), and AI-driven services.

- Number of Users: Around 224 million users globally, most of whom focus on the four main markets: Japan, Thailand, Taiwan, and Indonesia

- Revenue: $18 million monthly in-app purchase revenue as of August 2025

As initially a messaging app, LINE has evolved into a successful super platform and built its financial success on a highly effective product: digital stickers. Those expressive characters became a commercial language.

But the real super app move was the creation of the full ecosystem. LINE Pay allows for frictionless transactions, while its “Official Accounts” offer businesses and celebrities a direct line to their audience. This is a genius move for marketing.

8. Rappi (Latin America)

- Country of Origin: Colombia (serving Latin America)

- Key Features: Food delivery, grocery delivery, pharmacy, courier services (RappiFavor), digital payments (RappiPay), financial services, e-commerce, travel booking (RappiTravel).

- Number of Users: Over 35 million active users across Latin American countries, including Mexico, Brazil, and Colombia

- Revenue: Estimated $945.2 million in 2025

Switching continents entirely, we land in Latin America, and the undeniable leader is Rappi. Started out of Bogotá, Colombia, Rappi is often described as the “delivery everything” app that kind of just kept adding more layers to become a super app in Latin America.

The app’s real secret sauce is its incredibly versatile RappiFavor service. It’s not just food or groceries; you can essentially hire a runner to do anything, from walking your dog to fetching cash from an ATM for you. It’s a truly on-demand concierge service wrapped up in a delivery app. Plus, their digital wallet, RappiPay, is rapidly pushing cashless adoption in a region that, perhaps, hasn’t been as fast as Asia.

9. Shopee (Southeast Asia & LatAm)

- Country of Origin: Singapore

- Key Features: E-commerce marketplace (C2C and B2C), digital wallet (ShopeePay), integrated logistics (Shopee Xpress), live streaming/shopping (Shopee Live), food and grocery delivery (ShopeeFood/ShopeeMart), and in-app gamification.

- Number of Users: 295 million users

- Revenue: $4.3 billion in Q3 2025

Shopee is a genuine retail phenomenon across Southeast Asia, but it also manages to gain traction in some Latin American countries. It didn’t start out as a payments app that then added shopping, or a ride-hailing service that decided to deliver stuff; instead, Shopee went completely all-in on e-commerce first, and then started adding other crucial elements to truly transform into a super app.

Having said that, Shopee still focuses social commerce things. It makes shopping fun, giving out coins through gamification and running constant flash sales.

Besides, it deeply integrates Shopee Pay, its own digital wallet. It’s not just for paying for your new shirts or gadgets from Shopee’s e-commerce platform. You can use it to pay for actual utility bills, like electricity and water, outside the main marketplace. And, of course, like many top super apps in this list, you can order food and drinks through its service, ShopeeFood.

10. Tata Neu (India)

- Country of Origin: India

- Key Features: E-commerce (groceries, fashion, electronics), flight and hotel booking, financial services (loans, insurance), loyalty program integration across all Tata Group brands.

- Number of Users: 120 million users

- Revenue: Over $3.6 million in 2025

The Tata Group, which owns everything from Tetley Tea to Jaguar Land Rover to huge IT services firms, decided to create a single app, Tata Neu, to unify its vast retail empire. This is fundamentally different from a messenger (WeChat) or a payments app (Paytm) becoming a super app.

Tata Neu is trying to use the trust and loyalty built by decades of separate brands, like Air India, Taj Hotels, and Croma electronics, and put them all under one digital roof. One plus of Tata Neu is the NeuPass loyalty program, which rewards you for transactions across all of those services.

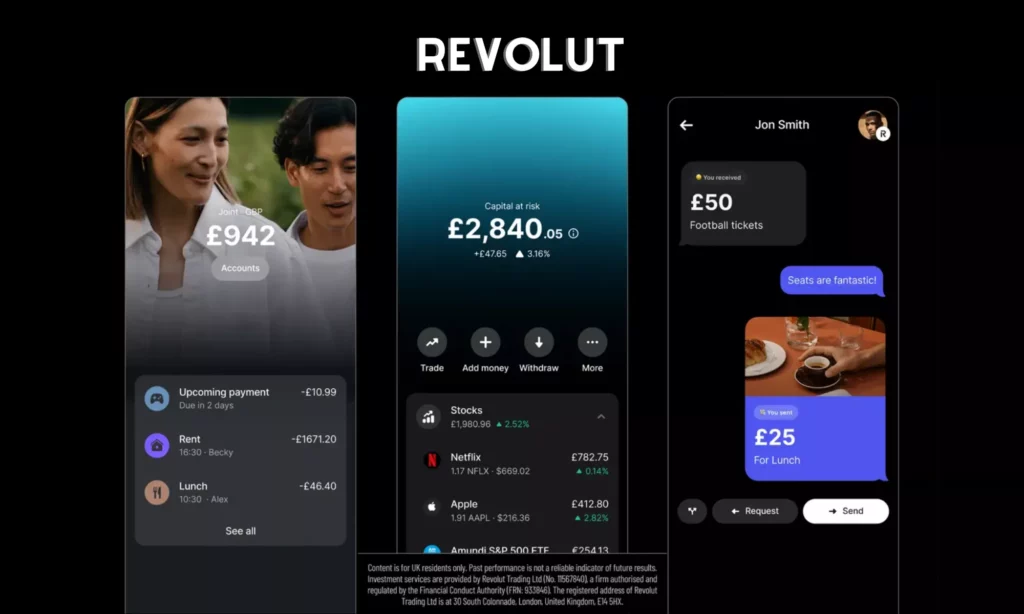

11. Revolut (Europe)

- Country of Origin: United Kingdom

- Key Features: Digital banking (current accounts, budgeting), currency exchange, stock trading, crypto trading, travel insurance, peer-to-peer payments, Revolut “Shops” (cashback and retail).

- Number of Users: Over 65 million customers globally

- Revenue: Approximately $1 billion in 2025

Revolut started from a financial base. Particularly, it offered a travel card service that helps people avoid foreign exchange fees, but it has then spiraled into a multi-service financial platform.

Revolut is not trying to do food delivery or ride-hailing itself, like other top super apps in this list. But it’s trying to be the financial operating system for your life. You’ve got your daily account, stock trading, crypto, business accounts, insurance – all in one slick, single app. Its aggressive push into new territories and its constantly expanding suite of financial products, like its retail cashback program, strongly suggest a super app mindset, albeit one focused squarely on finance and commerce.

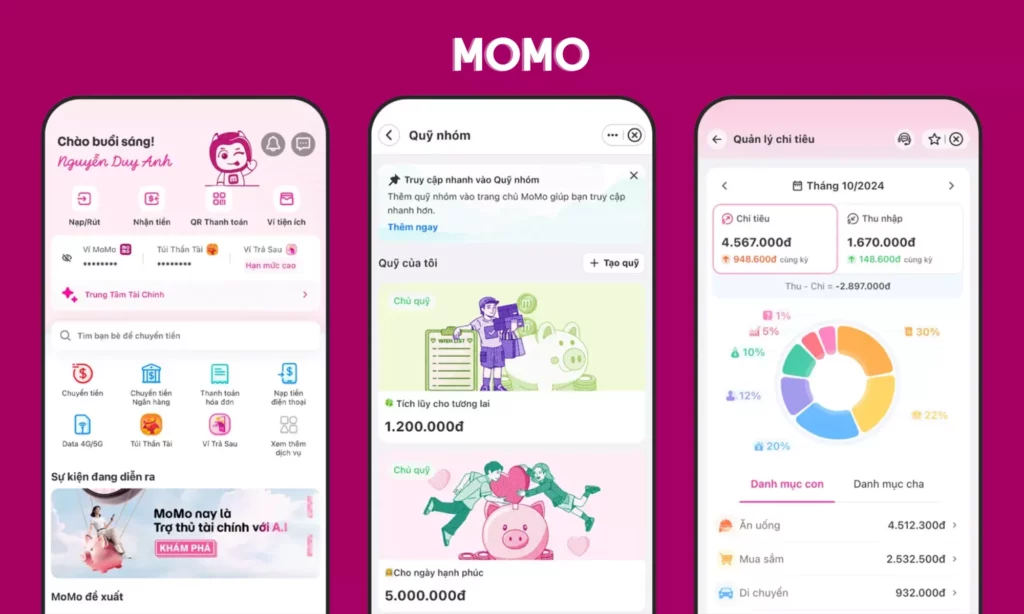

12. Momo (Vietnam)

- Country of Origin: Vietnam

- Key Features: Mobile payments (e-wallet and QR code), bill payments, money transfer, mobile top-ups, ticketing (movies, transport), insurance, financial services (P2P lending, investments), and a marketplace for mini-applications.

- Number of Users: Over 30 million registered users in 2025

- Revenue: Around $482 million in 2024

If you’re looking for the Vietnam-based Vietnamese super app, don’t ignore Momo. The app started primarily as a digital wallet, focusing on cashless transactions and bringing financial inclusion to the public.

Today, MoMo is so much more than just a mobile payment solution; it’s practically a financial dashboard. Momo, of course, lets you transfer money to bank accounts, pay for orders by scanning QR codes, and make automated payments for utility bills. Besides, it offers financial services, like cash deposit and money lending. What makes Momo striking is its AI financial advisor, which helps you manage monthly spending and make smart investments.

13. Zalo (Vietnam)

- Country of Origin: Vietnam

- Key Features: Instant messaging (text, voice, video), social networking, Official Accounts for businesses and government services, mini-apps/utilities (ZaloPay for payments, news, weather), and file sharing.

- Number of Users: Over 78 million monthly active users in Vietnam

- Revenue: Estimated $413.15 million in 2025

While MoMo took the financial route, Zalo took the communication route. This Vietnam-based app is really the local equivalent of WeChat or LINE in its dominance of the messaging space.

The magic happens when you look beyond the chat feature, though. Zalo has smartly integrated a whole universe of services, including ZaloPay, which is a key rival to MoMo. More importantly, it features “Official Accounts” that let businesses, and even government bodies, communicate directly with users, which is a huge convenience factor.

Zalo also proves itself as a truly super app with its seamless integrations of a game center, a financial tool (Fiza), and Zalo short videos. Further, it allows you to access a wide range of on-demand mini apps for shopping, finance management, car booking, job hunting, and even tarot card reading.

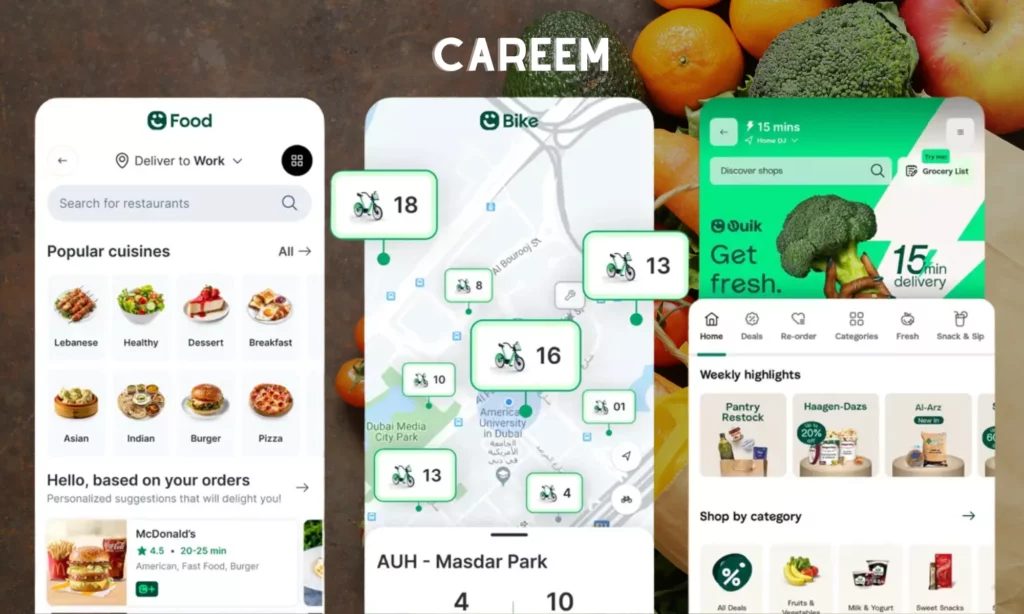

14. Careem (Middle East)

- Country of Origin: Dubai, UAE (serving the Middle East, North Africa, and South Asia)

- Key Features: Ride-hailing, food delivery, package delivery, peer-to-peer credit transfer, utility bill payments, booking third-party services (cleaning, laundry).

- Number of Users: Over 50 million registered users across its regions

- Revenue: A subsidiary of Uber since 2020, Careem’s financial contributions are folded into Uber’s Middle East operations. Revenue is primarily derived from its mobility and delivery commissions.

Originally a major competitor to Uber in the Middle East, Careem was ultimately acquired by them. But it has maintained and expanded its super app strategy ever since. Operating across 13 countries, they are the go-to app for life in that dynamic, mobile-first region.

Careem doesn’t just focus on transport, though that’s the foundation. Careem has pushed heavily into the financial side – you can use its wallet to pay utility bills, transfer credit to friends, and access a growing marketplace of local services, which is pretty critical in high-density urban areas. It’s effectively building a digital ecosystem tailored specifically for the MENA user, which often means handling cross-border complexities and local service fragmentation.

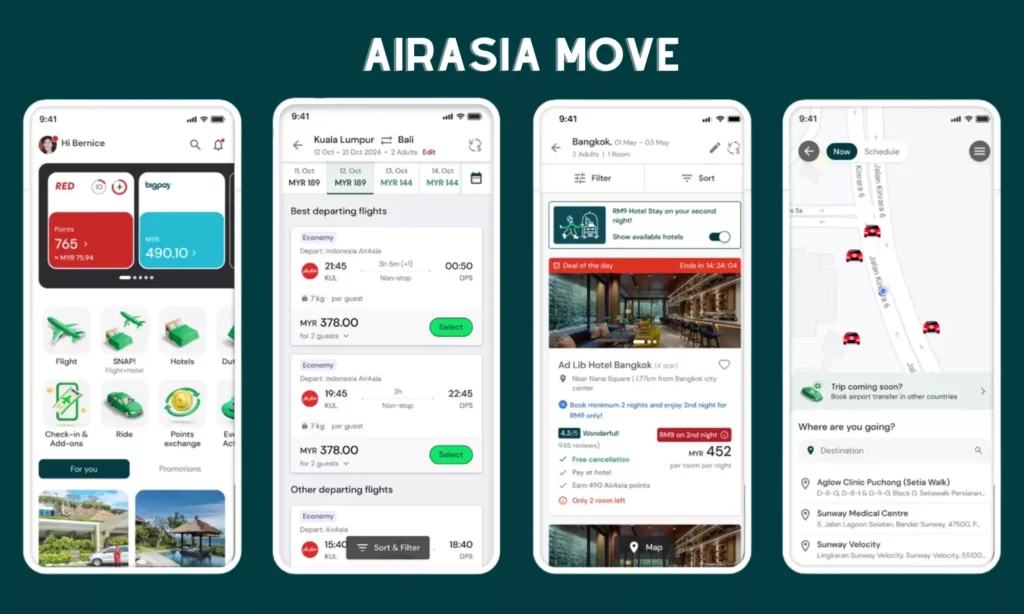

15. AirAsia MOVE (Malaysia)

- Country of Origin: Malaysia

- Key Features: Airline ticket booking (its core), hotel reservations, flight + hotel bundles (SNAP), ride-hailing (AirAsia Ride), food delivery (AirAsia Food), package delivery (AirAsia Express), and financial services via its sister entity, BigPay.

- Number of Users: Over 15 million monthly active users

- Revenue: Around $27 million in 3Q25

The last, and also a very different super app in our list, is AirAsia MOVE. AirAsia was initially a low-cost airline, but it then made a hard pivot and decided to become a super app to survive the challenges of the travel industry, especially after the pandemic. Now, you can book a flight, a hotel, hire a car to the airport via AirAsia Ride, and even order food, all in one place.

How Designveloper Helps Develop Successful Super Apps

So, we’ve talked about the titans: WeChats, Grabs, Paytms, and many more. It’s clear the super app model is a phenomenal business opportunity, but building one is an incredibly complex undertaking. This is where Designveloper, a leading software development and IT consultation company, steps in as a trusted partner alongside your development journey.

You might have a great core service – let’s say, a travel booking app – but expanding that into a full super app requires careful planning to ensure those new services feel genuinely seamless, not just tacked on. So, we’ll start with in-depth IT consultation to map out your core use case, identify high-impact service additions (the ones that really drive daily user retention), and build a clear, phased development roadmap.

We actually focus heavily on the ‘micro-frontends’ and modular architecture that let you launch new features and onboard third-party partners independently without risking the stability of the entire platform. We also understand the importance of the UI/UX design. That’s why we focus on building an intuitive interface and mapping out complex user journeys to make the transition between different services smooth.

With our proven Agile approaches, technical excellence, and proactive communication, our team empowers you to build not just an app, but a self-sustaining digital solution. Contact us now and start realizing your idea!

FAQs About Super Apps

Is TikTok a Super App?

Nope. TikTok is superficially developing into a super platform, with its expansion into e-commerce (TikTok Shop). However, it still integrates the key features of social media and mainly offers short-form videos. Further, it’s not a “closed ecosystem of many mini apps,” which is considered an exact definition to describe a super app.

What is the Largest Superapp in The World?

WeChat can be considered the largest super app globally, based on the number of monthly active users we discussed above (around 1.4 billion) and revenue ($62 billion). The app has an upper hand in its main user base, which includes mostly China-based people. Focusing on communication and payments, it offers a vast bank of mini-programs.

What is The Secret of Super Apps?

The main secret of super apps is a seamless combination of some integral components. First, they must have a strong core use case that guarantees daily use, whether messaging, payments, or ride-hailing. Second, they must have seamless integration with digital wallets to remove all friction from transactions. Finally, they smoothly connect third-party services (Mini Programs or API partnerships) to scale their offerings infinitely without having to build every service themselves.

Are Super Apps Profitable?

Yes, generally speaking, the most successful and largest super apps are profitable, though sometimes the parent company might invest initial profits back into aggressive expansion. They are powerful revenue-generating machines precisely because of their scale and multi-functionality.

Their revenue streams don’t just come from one thing but rely on various services. They often employ a hybrid model of monetization, including commission-based revenue (from every ride, food order, or ticket sale), advertising (leveraging all that granular user data for highly targeted ads), and financial service fees (from lending, wealth management, or cross-border payments).

This multi-pronged approach helps them sustain profitability even with high operating costs, which is actually a key reason why single-purpose apps often struggle against them.

{kind=link}